.svg)

.png)

In today's dynamic financial landscape, credit scoring acts as a backbone in assessing the financial health of individuals and businesses alike. As technology grows, the way we figure out someone's credit score gets fancier too. It's like upgrading to a smarter system for keeping track of how good someone is with money. This helps in making fair decisions about loans and stuff.. As industries adopt digital transformations, credit scoring systems must adapt to ensure accurate risk assessments. This blog delves into the complexities of credit scoring with the current industry trends.

In this dynamic environment, Nected takes center stage as a modern, adaptive, and user-friendly credit scoring solution. It seamlessly integrates technology and financial senses, catering to the diverse needs of industries relying on credit scoring systems. Nected's approach aligns with the ever-changing demands of the digital age, offering a comprehensive and efficient solution to the challenges posed by the traditional credit scoring methods.

This blog aims to unwind the layers of credit scoring, exploring its nuances, and illuminating the path to a modern approach with Nected. Join us on this insightful journey as we navigate through the domain of credit scoring platforms, systems, software, and score platforms, shedding light on the transformative power of Nected in this crucial financial domain.

Exploring Credit Scoring: An In-Depth Overview

Credit scoring is a sophisticated mechanism used by financial institutions to evaluate the creditworthiness of individuals and entities seeking financial services. It revolves around the meticulous analysis of various factors to generate a numerical credit score. This score serves as a standardized metric, aiding lenders in making informed decisions about extending credit.

Significance in Financial Assessments

The significance of credit scoring in financial assessments cannot be overstated. It serves as a linchpin in the decision-making process for lenders, offering a systematic and objective approach to evaluating the risk associated with providing credit. By delving into an individual's credit history and financial behavior, credit scoring provides a comprehensive picture that helps lenders mitigate risks effectively.

Types of Credit Scoring

Credit scoring comes in diverse forms, catering to the specific needs and contexts of different industries and institutions. Two primary types include:

- Generic Credit Scoring: This approach applies a standardized set of criteria to assess creditworthiness, making it suitable for a broad population.

- Custom Credit Scoring: Tailored to specific industries or institutions, custom credit scoring accommodates unique criteria that may be more relevant to certain contexts.

Primary Components of Credit Scoring

Understanding the intricate nature of credit scoring involves delving into its primary components:

- Payment History: A detailed examination of an individual's track record in meeting credit obligations over time.

- Credit Utilization: Analysis of the ratio of credit used to the total available credit, providing insights into responsible financial behavior.

- Length of Credit History: Consideration of the duration of an individual's credit accounts, reflecting stability and experience in handling credit.

- Types of Credit in Use: Assessment of the variety of credit accounts held, offering a glimpse into the diversity of an individual's credit portfolio.

- New Credit: Evaluation of recent credit inquiries and account openings, helping lenders gauge recent financial behavior.

These are some basic parameters that are assessed while calculating credit score. However, more parameters can be used to calculate credit score such as recent credit behavior, available credit etc. By exploring the intricacies of credit scoring and understanding its components, individuals and businesses can navigate the financial landscape with greater awareness and confidence. Stay with us as we delve deeper into the transformative power of credit scoring.

Industries and Functions Leveraging Credit Scoring

Credit scoring is not confined to the realm of finance alone; its far-reaching impact extends across various industries and functions, revolutionizing decision-making processes. Let's explore how different sectors leverage credit scoring to make informed choices:

- Banking and Finance:

In the financial sector, credit scoring is the backbone of lending decisions. Banks and financial institutions utilize credit scores to assess the risk associated with providing loans or credit cards. This ensures responsible lending practices and helps you make better lending decisions.

- Insurance:

Insurance companies employ credit scoring to evaluate the risk profile of potential policyholders. Credit-based insurance scores assist insurers in determining premium rates and coverage eligibility. Individuals with favorable credit scores may enjoy lower insurance premiums.

- Retail:

In the retail sector, credit scoring is employed for customer relationship management. Retailers may use credit scores to determine credit limits for store credit cards or installment plans. This facilitates personalized shopping experiences while managing credit risk.

- Real Estate:

Credit scores play a pivotal role in real estate transactions. Mortgage lenders use credit scores to evaluate the creditworthiness of homebuyers. A higher credit score often leads to more favorable mortgage terms and lower interest rates.

- Employment Screening:

Certain industries incorporate credit scoring into their hiring processes. For positions involving financial responsibilities, employers may consider an applicant's credit history as part of the screening process. This is particularly relevant in roles where financial trustworthiness is crucial.

Real-world Examples

- Auto Financing: Car dealerships often rely on credit scores to assess an individual's eligibility for auto financing. A higher credit score may result in more favorable loan terms and lower interest rates.

- Telecommunications: Some mobile service providers use credit scoring to determine whether customers qualify for postpaid plans or need to opt for prepaid options.

- Utilities: In some regions, utility companies may consider credit scores when determining whether to require a security deposit for new service connections.

By delving into these real-world examples, you gain insights into the diverse applications of credit scoring. The universality of its impact reflects the versatility and importance of credit scoring mechanisms in today's multifaceted business landscape. Stay with us as we further explore the problem-solving prowess of credit scoring.

What Problems Does Credit Scoring Solves?

Credit scoring is more than just a numerical evaluation; it's a powerful tool designed to address a spectrum of challenges faced by businesses and individuals alike. Let's delve into the specific problems that credit scoring solutions aim to solve:

Business-End Problems

- Risk Mitigation: Credit scoring serves as a robust risk mitigation strategy for businesses, especially those in the financial sector. By assessing the creditworthiness of customers, lenders can make informed decisions on loan approvals, reducing the risk of defaults and financial losses.

- Efficient Decision-Making: For financial institutions and lending organizations, timely and efficient decision-making is paramount. Credit scoring streamlines this process, enabling swift assessments of loan applications. This not only improves operational efficiency but also enhances the overall customer experience.

- Portfolio Management: Credit scoring facilitates effective portfolio management for banks and financial entities. It allows these institutions to diversify their portfolios based on varying risk levels associated with different credit scores. This strategic approach helps optimize profitability and minimize potential losses.

Customer-Centric Issues

- Access to Credit: One of the primary challenges customers face is obtaining access to credit. Credit scoring addresses this by providing a standardized method for assessing creditworthiness. Individuals with favorable credit scores are more likely to secure loans and financial products with reasonable terms.

- Fairness and Objectivity: Credit scoring introduces fairness and objectivity into lending decisions. Unlike subjective assessments, credit scores are based on quantifiable data, ensuring that individuals are evaluated impartially, solely based on their financial history and behavior.

- Interest Rates and Terms: Customers with higher credit scores often enjoy preferential interest rates and more favorable terms. This incentivizes responsible financial behavior, creating a symbiotic relationship where customers benefit from lower costs, and lenders mitigate risks.

By addressing these business-end and customer-centric problems, credit scoring emerges as a valuable mechanism that promotes financial stability, responsible lending, and equitable access to credit opportunities. Stay with us as we explore the core technicalities behind the implementation of credit scoring solutions and also how Nected stands out in this domain.

Core Technicalities of Credit Scoring Implementation

Now that you've gained insights into the fundamental significance of credit scoring, let's navigate the core technicalities associated with its implementation. Understanding these technical aspects is crucial for grasping how credit scoring models operate and deliver actionable insights.

Key Parameters and Considerations

- Credit Score Range: Understanding the score range is essential. Typically, higher scores indicate lower credit risk, while lower scores suggest a higher risk.

- Weightage of Factors: Different factors contribute differently to the credit score. For instance, payment history and outstanding debts often carry significant weight.

- Scalability: The credit scoring model should be scalable to handle a large volume of data efficiently, especially for institutions dealing with numerous credit applications.

- Regulatory Compliance: Adhering to legal and regulatory standards is imperative to ensure fairness, transparency, and ethical use of credit scoring algorithms.

As you explore the intricacies of credit scoring, stay tuned to know how Nected seamlessly integrates these technicalities, offering a modern and effective credit scoring solution.

Implementing Credit Scoring with Nected: A Step-by-Step Guide

Embarking on the journey of credit scoring implementation becomes streamlined and efficient with Nected. This low-code, no-code rule engine empowers you to construct and deploy credit scoring models without the need for extensive coding which is compulsory when building credit scoring in house.

Here's a step-by-step guide on how to leverage Nected for credit scoring:

Step 1: Navigating the Nected Interface

Login to the intuitive Nected platform. The user-friendly interface ensures a smooth start for both seasoned professionals and those new to credit scoring.

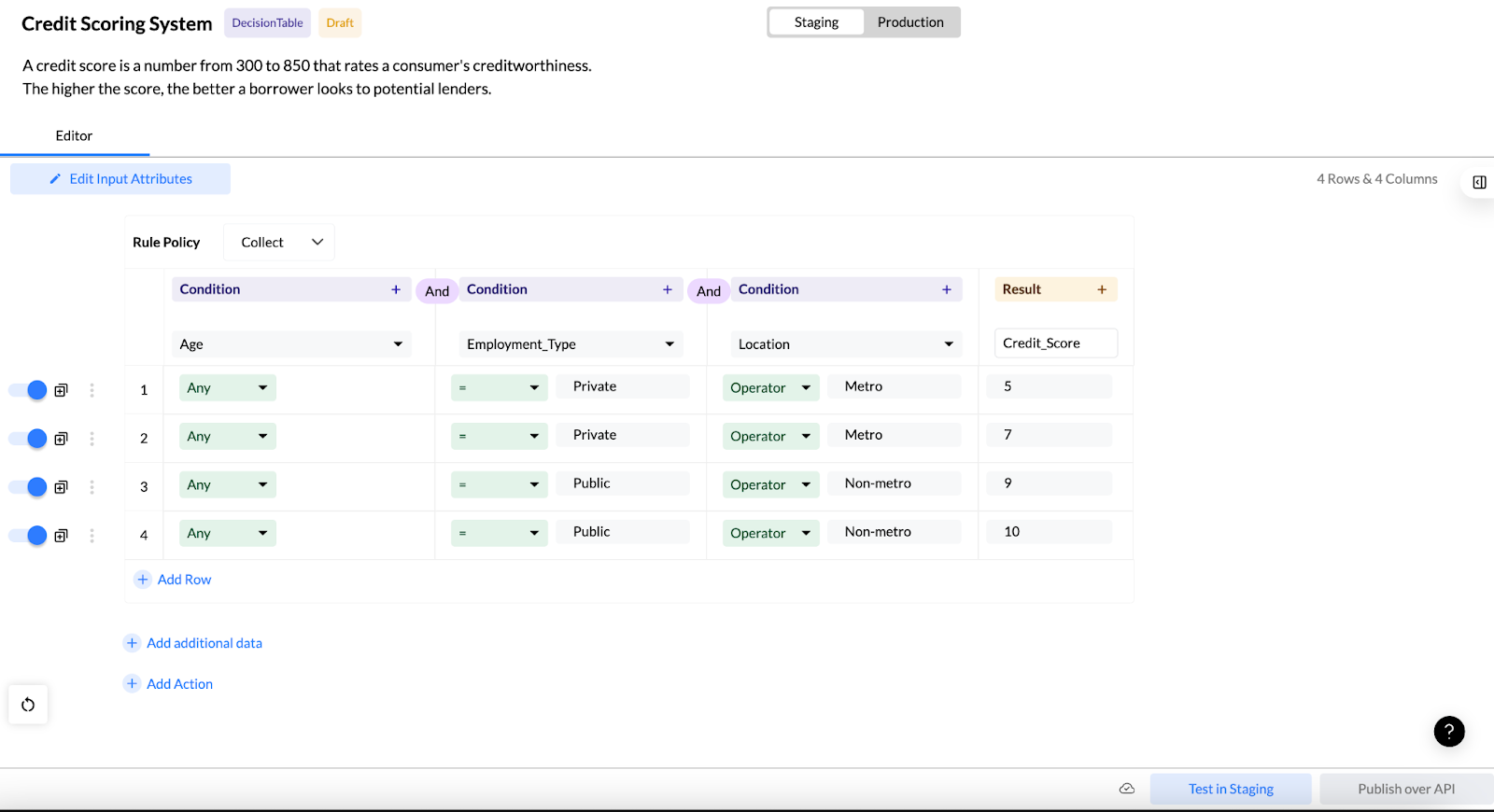

Step 2: Create a New Rule for Credit Scoring

Create a new rule within Nected dedicated to your credit scoring endeavor. Define the project scope, objectives, and the specific parameters you wish to include in your credit scoring model.

Step 3: Integrate your data with more than 100 connectors available.

Seamlessly integrate diverse data sources into Nected. Whether it's financial histories, payment behaviors, or other relevant information, Nected accommodates a variety of data, ensuring a comprehensive approach to credit scoring.

Step 4: Rule-Based Model Creation

Now, add input attributes such as age, employment type, taxable income or any other parameters that you want to build your credit scoring rule set upon.

Click Save & Next and now let's move on to creating rules for credit scoring.

Leverage Nected's rule-based approach to craft credit scoring models. Define rules based on the selected features and parameters. Nected's low-code environment facilitates rule creation without the need for intricate coding skills.

Step 5: Testing and Validation

Test the credit scoring model within Nected using your data. Validate the model's accuracy and reliability, ensuring it aligns with the expected outcomes.

Step 6: Deployment

Once satisfied with the testing phase, seamlessly deploy your credit scoring model through Nected. The platform's deployment capabilities ensure a swift transition from development to practical application.

Watch this video to get more deeper insights on creating credit scoring rules with Nected.

Why use Nected as a Credit Scoring Platform?

- Efficiency: Nected streamlines the credit scoring process, reducing the time and effort traditionally required for model development.

- Customization: Tailor credit scoring models to your specific needs with Nected's customizable rule creation, allowing for a personalized and adaptable approach.

- Scalability: Nected is designed to handle varying data volumes, making it an ideal solution for institutions dealing with numerous credit applications.

- Rule Transparency: Gain insights into the credit scoring decision-making process. Nected's low-code, no-code rule-based approach ensures transparency and a clear understanding of how credit scores are derived.

- User-Friendly Interface: Nected's user interface is designed for accessibility, ensuring that professionals across different expertise levels can engage with the platform seamlessly.

By adopting Nected for credit scoring implementation, you embrace a modern and efficient solution that combines advanced capabilities with user-friendly design.

Tool Comparison: Nected vs. Alternatives for Credit Scoring

Choosing the right credit scoring tool is paramount for effective financial assessments. Let's compare Nected with other tools available in the market to help you make an informed decision:

Choosing the right credit scoring platform is a critical decision that hinges on specific business needs, data integration requirements, and the adaptability demanded by the ever-evolving financial landscape.

Nected's low code no code approach aligns with the demands of modern businesses, providing a robust and flexible solution for effective credit scoring. As industries continue to evolve, having a credit scoring platform that can seamlessly integrate into the business processes is paramount, and Nected emerges as a contemporary choice for achieving that synergy.

Dive into the world of credit scoring with Nected and unlock new possibilities for your business.

Conclusion

Navigating the intricate domain of credit scoring demands a thoughtful consideration of various platforms, each offering its unique blend of features and functionalities. As you explored the landscape, it became evident that Nected, with its low-code, no-code rule engine, is well-positioned to meet the diverse needs of businesses. The flexibility, adaptability, and user-friendly nature of Nected make it a standout choice in the dynamic world of credit scoring.

Choosing the right credit scoring solution is pivotal for businesses aiming for precision and efficiency in financial assessments. Nected not only addresses the complexities associated with credit scoring but also presents an innovative and modern approach to rule-based engines. The seamless integration, adaptability to evolving patterns, and user-friendly design set Nected apart, making it an optimal choice for businesses seeking a reliable credit scoring platform.

FAQs

Q1. What makes credit scoring essential for businesses?

Credit scoring is crucial for businesses as it provides a systematic and data-driven approach to assess the creditworthiness of individuals and entities. By evaluating financial behaviors and patterns, businesses can make informed decisions, mitigate risks, and maintain healthy financial operations.

Q2. Can Nected be customized to suit unique business needs in credit scoring?

Absolutely. Nected's versatile design allows businesses to customize credit scoring models based on their specific requirements. Whether it's adjusting parameters, incorporating industry-specific elements, or evolving with changing patterns, Nected provides a tailored solution for diverse business needs in credit scoring.

.svg)