.png)

.webp)

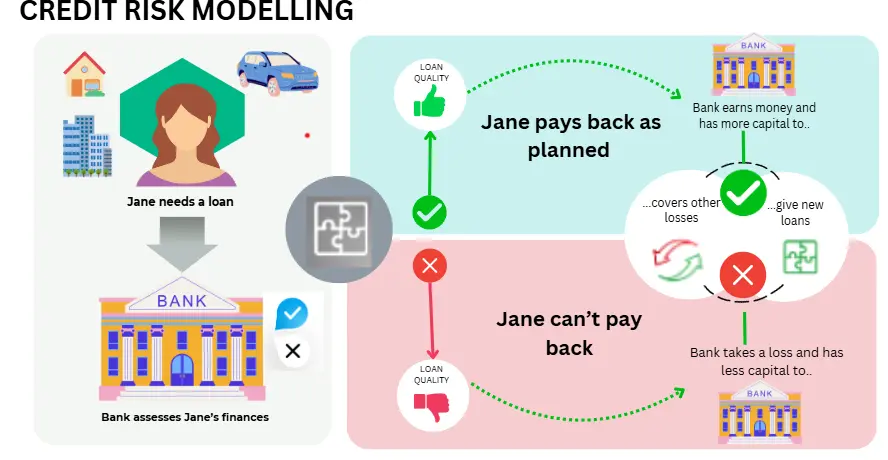

Counterparty credit risk is commonly defined as the possibility that the counterparty, or the other party to a certain financial transaction, will be unable to fulfill his contractual obligations. This type of risk is usually common in products like derivatives, securities lending and foreign exchange whereby both contract parties rely on the counterpart to deliver his side of the bargain. Counterparty credit risk is a major problem in the financial market since in the case of default, one party suffers financial losses.

In financial markets, counterpart credit risk is significant since it affects the stability as well as the confidence of the participants in the market. Banks, investment banks, trading companies, and clearinghouses are a few examples of financial institutions that conduct numerous transactions daily. When counterparties fail to fulfill their contractual obligations, it triggers chain effects, instantly resulting in a lack of liquidity, loss of capital, and possibly, systemic failures. It is crucial to mitigate this risk to avoid drastic fluctuations in the market and maintain its stability.

In addition to the actual credit loss, there are other risks when a counterparty is unable to meet its obligations. This outcome can result in legal actions, negative word of mouth and contractual constraints in the market. Also, a default can create a snowball effect, most especially if the entities defaulting are related in one way or the other through various financial derivatives. This was evident in the 2008 financial crisis where counterparty risks caused the world to be hit hard with an economic collapse and that urged institutions to embrace efficient measures to manage such risks.

For the management of counterparty credit risk, credit risk analysis and therefore, credit risk modeling is crucial. Nected, a low code/no code platform that offers modern, best-in-class rules based engine and workflow orchestration functionality allow businesses to set up efficient risk management solutions. Through the use of Nected, organizations can be able to fully manage the credit risks without having to invest in technical knowledge to do so, thus enhancing security from counterparty risk.

Create credit scoring models for enhanced risk management. Try Nected today!

What is credit risk analysis?

Credit risk analysis is the process of determining the probability of a borrower or a counterparty defaulting on the payment of his/her/its dues. Upon the identification of the criteria, data takes a significant part in this process because it constitutes the basis on which the possibility of a counterparty’s financial distress can be estimated. Banks and other such financial entities assess the risk level tied to each counterparty by analyzing historical information, transactions, balance sheets, and the current market state. This analytical technique makes it possible to have greater accuracy as to perceived risks within the environment of the financial market, to make informed decisions on who to potentially interact with in business.

What is Credit Risk Modelling?

Credit risk modeling is the technique of assessing the probability of non performance of a counterparty obligation. These models are used to calculate probable credit losses through aspects such as credit history, market data, and past and existing financial performance. Credit risk models can be used as helpful tools for the evaluation of counterparty risk and decision-making process in concerns with lending or trading.

How credit risk models help assess potential credit losses?

Credit-risk models enable institutions to estimate the likely credit exposures of default for a counterparty. This way the models are able to predict the probability of default (PD), loss and given default (LGD), as well as the exposure at default (EAD) by considering factors that include credit ratings, loan-to-value ratios, and market volatility. This makes it possible for the businesses to evaluate the degree of loss in the case of default and review their strategies of risk management.

Different approaches to credit risk modeling

There are several approaches to credit risk modeling, each with its own methodology:

Structural models: These are based on balance sheet values to consider the possibility of default taking into account the firm’s assets and liabilities.

Reduced-form models: These use credit risk to estimate probability of default without reference to balance sheet details but from market data including credit spreads.

Machine learning models: These models are gaining popularity, employing large data sets and statistical methods to detect and forecast defaults more efficiently.

Rules based models: These models make use of a predetermined set of rules related to financial history, to assess the probability of default to return the asset to the lender.

Read Also: Credit Risk Assessment Guide: Strategies for Effective Credit Risk Monitoring

The Importance of Managing Counterparty Credit Risk

One example of counterparty risk reaching disastrous levels is the situation that unfolded with Lehman Brothers in 2008. Failure of Lehman marked a series of disaster funds that affected the world financial systems since it left many institutions in great losses due to their involvement with Lehman on the derivatives and lending assets. The other example can be named the default that had occurred in the situation with Enron in 2001, when various counterparties who worked with the company experienced significant financial pressure due to its failure. These cases show that the credit risks can result in large scale instability if a counterparty is unable to meet its obligations.

Role of counterparty risk in global financial stability

Obviously, counterparty risk plays a crucial role to sustain global financial stability. The problem with financial institutions for which the failures of one counterparty impose the risk of a series of failures is that it results from liquidity squeezes and fear of default. The mitigation of counterparty risk means that any disruptions to this kind of services are reduced and this boosts confidence in the financial markets. Reducing counterparty risks thus plays a vital role in maintaining stability of the overall economy and avoiding any negative domino effect in the institutions.

How can businesses mitigate counterparty risk?

Counterparty risk can be reduced by using modern technological tools that provide complex credit risk evaluation with ease such as Nected. Nected’s rule-based engine enables institutions to effectively define creditworthiness of counterparties and swiftly alert on potential risks. Furthermore, thorough risk assessment can be made through implementing the concept of workflow orchestration, which lessens the probability of errors that may be committed through human intervention and addresses difficulties in responding to new threats on time. Thus, it contributes to avoiding contact with high-risk counterparts and limiting possible losses.

Read Also: Essential Risk Management Techniques in 2024

Building Effective Credit Risk Models with Nected

Low-code/no-code capabilities of the Nected include automated integration of credit risk models through its user-friendly tools such as the workflow manager and rules engine. Here's a step-by-step breakdown:

Data Integration: The first phase can therefore be described as data importation, which is the entry of key data into Nected. This could include credit information of the counterparties, financial information that includes the balance sheet, income statement, cash flow statement, transaction history, and other market data. Nected can extend with different information sources by APIs or by the uploading of datasets which, in turn guarantees that the model receives all relevant data for risk evaluation.

Defining Risk Parameters: Other sensitive risk factors like Probability of Default (PD), Loss Given Default (LGD) and Exposure at Default (EAD) are specified by using the rules engine of the platform. These parameters are also the basis of the credit risk model and using them the model can estimate possible credit losses for each counterparty. Finally, Nected’s rule-base system allows the setting of these parameters without having to write codes, thus can easily be controlled by users who do not have the technical know-how in programming.

Workflow Orchestration: After the rules have been set, the workflow manager then coordinates the movement of the credit risk evaluation process. Using conditional settings, users can work with a graphical interface to visually design the workflow of data processing and rule application to each counterparty. For instance, it is possible to set specific rules through which counterparties that are associated with predefined risk levels are marked and this is followed by notifications and further evaluation.

Automated Risk Assessment: Once the workflows are set up, Nected then automates the assessment of credit risk. In terms of credit risk management the platform is constantly comparing counterparty data and feeding the rules set in the model to see if there is a change in risk exposure. This type of evaluation offers businesses current assessment of counterparty risks and enables them to act on any emerging risk factors.

Adjusting Models Over Time: Since credit risk environments can change, Nected’s user friendly approach allows users to adapt its models to the situations they encounter when using the program. Hence when market conditions change or new data is available to be incorporated, users are able to alter the risk rules and workflows easily without much harassment as to technicality thus making the risk management system more dynamic.

With Nected, the process is made as easy as you can imagine. Automate your credit scoring models easily with Nected.

Benefits of Using Nected’s Low-Code/No-Code Platform for Credit Risk Modeling

There are several benefits associated with using Nected for credit Risk Models. Below are some most common benefits:

Accessibility: Business users can build and edit credit risk models, and it will not require any programming knowledge, thereby minimizing dependence on tech support.

Speed: The main advantage of using this platform is that it allows for faster creation and deployment of risk models due to the presence of a drag-and-drop function for creating applications.

Scalability: Nected enables credit risk models in businesses to grow with the operation and easily handle complex processes and massive datasets without compromising on efficiency.

Flexibility: The risk parameters and the related work processes can then be easily modified based on the market conditions or new data available so that the risk models stay valid.

Automation: Nected centralizes the management of credit risk, analyzing counterparties and adjusting risk indicators in real-time.

Cost-Efficiency: Nected definitely comes out as cheaper to implement than conventional credit risk modeling models since fewer codes and manual procedures are necessary.

Compliance Support: Integration with other modules allows the use of pre-designed work flows for compliance with the requirements of the credit risk regulation to different businesses depending on their field of activity.

Read Also: Top 7 Risk Management Tools For Businesses

How Credit Risk Analysis Supports Better Financial Decisions

Some points which prove that Credit risk analysis supports financial decisions & stability are as follows:

Identifies High-Risk Counterparties: Credit risk analysis assists businesses find out counterparties that may fail to meet their obligations hence enabling businesses not to transact with entities that may bring havoc to their financial status.

Provides Data-Driven Insights: Through looking at historical and real time information, credit risk analysis is therefore beneficial in helping businesses gain better understanding of their counterpart’s credit worthiness thereby coming up with better decisions.

Improves Loan Portfolio Management: Credit risk analysis enables organizations to properly assess the risky loans that are in the loan books so as to properly channel the right resource to the right direction.

Supports Proactive Risk Management: Conducting credit risk assessments on a regular basis helps companies to identify risks and intervene in advance, for instance, adjusting credit limits for specific parties.

Enhances Investor Confidence: Having a strong credit risk management also increases the confidence of investors and stakeholders when carrying out their operations they are assured that the business is doing everything possible to protect their financial interests.

Optimizes Pricing Strategies: Through assessing the credit risk of each counterparty, firms can change their organizational strategies such as offering better terms for low-risk credit clients as well as pricing more risks for the less reliable counterparties.

Enables Strategic Growth Decisions: Credit risk management enables organizations to make informed decisions for their growth, by expanding in areas they know have credit risks, or investing in assets they understand have credit risk.

Strengthens Regulatory Compliance: Credit risk evaluation with focus on a wide range of factors is an efficient way to prevent legal violations that can lead to fines concerning the absence of sound credit risk management.

Conclusion

Counterparty credit risk is an important factor in determining the outcomes of financial operations, as the default of a counterparty can result in substantial losses. Therefore, it is critical to grasp this risk, control it and minimize it for organizations that want longevity. By credit risk analysis and credit risk modeling, the risks can be evaluated, decisions made, and financial health of the organization preserved. Based on such sophisticated models and time-variant data, companies can predict the likelihood of counterparty risk failures and counteract accordingly to minimize potential losses.

Nected, with the help of its low-code/no-code platform, enables the easy and efficient creation and management of credit risk models. Their workflow manager and rules engine enable credit risk models to be designed and implemented in a simple manner leading to better financial decisions with minimal need for any technical assistance.

FAQs

Q1. What are the two types of counterparty risk?

Pre-settlement risk and settlement risk are the two key types of counterparty risk that exist in the field. Pre-settlement risk is defined as the risk that any of the counterparties involved in a transaction will fail to fulfill their contractual obligations prior to the completion of the transaction. This risk can be due to movements in the markets or otherwise some form of insecurity. On the other hand, settlement risk arises when one counterparty performs while the other counterparty does not perform after the transaction has been opened but before it is closed.

Q2. What is the difference between CVA and CCR?

Credit Valuation Adjustment (CVA) and Counterparty Credit Risk (CCR) are closely related concepts, but they serve different purposes. While CVA and CCR may seem similar, they are fundamentally used for distinct objectives. Credit risk in this case is defined as the probability that a counterparty to a financial contract will fail to honor his or her obligations, resulting in losses for the other contracting party. But CVA is the adjustment to the value of a derivative, or a financial instrument for the credit risk of the counterparty. In effect, CVA is the cost of counterparty risk when factored into the price of a transaction and CCR is default risk in general.

Q3. What is CCR in banking?

CCR in banking means the exposure of a financial institution to the risk of a counterparty in a given transaction like loan, derivative contract or trade not meeting his contractual obligations. This type of risk is especially relevant for contracts that entail financial contracts such as derivatives or other contracts developing at a certain date in the future. Banks face this risk whenever they engage clients in contracts and it is up to them to calculate this risk by implementing adequate risk models, collateral and real-time monitoring to contain potential losses.

Q4. How to measure counterparty credit risk?

Counterparty credit risk is estimated in different ways and with help of many models and factors, the most common of them being Probability of Default (PD), Exposure at Default (EAD) and Loss Given Default (LGD). These metrics are used to determine the chances of the counterparty defaulting, the amount of exposure at the time of default and the expected loss at the time of default. Further, the actual and expected losses are calculated using sophisticated credit risk models like the Monte Carlo simulation or scenario analysis to arrive at potential credit exposure at a given market condition. In any case, proper measurement also requires monitoring of counterparties’ creditworthiness and market trends on a regular basis.

Q5. What are the 5 components of credit risk analysis?

The five Cs of Credit include – Character, Capacity, Capital, Collateral, and Conditions and the lender uses it to evaluate the credit worth customers. Character focuses on the ability of the borrower to repay the money honestly, Capacity analyzes the borrower’s capability of repaying the loan, Capital checks on the collateral that the borrower has put up for the loan, and Conditions are factors that may influence the repayment of the loan.

.webp)

.svg.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)