.png)

.webp)

Understanding a credit scoring model matters more than most people think. Lenders use it to judge risk, set terms, and decide whether a borrower gets approved at all. If you work with lending, underwriting, or even product decisions around credit, this part usually gets ignored until it starts causing trouble.

Different types of credit scoring models are used for different jobs. Some are old-school and heavily tied to payment history. Others pull in behavioral data or machine learning signals. And yes, the model a lender chooses can change the outcome pretty quickly.

That is where platforms like Nected come in. It uses a rules-based approach that works well with credit decisioning workflows and modern scoring logic. If you are comparing credit scoring software or looking at an open source credit scoring platform, the moving parts start to look familiar fast.

What Is a Credit Scoring Model?

A credit scoring model is a system used to estimate how likely someone is to repay a loan or meet other credit obligations. It takes financial data, applies scoring logic, and turns it into a number or a decision. Simple on paper. This part often gets ignored, but the data choice behind the model changes everything.

Some models rely on classic bureau data. Others bring in income patterns, spending behavior, or non-traditional signals. That difference is what separates a basic score from a more flexible credit risk model.

How Credit Scoring Models Work

Most models follow the same rough flow. They collect borrower data, clean it, score it against predefined rules or learned patterns, and produce a risk outcome. Lenders then use that result to approve, decline, or adjust terms.

Traditional systems use fixed factors like payment history and credit utilization. Machine learning models do more pattern matching across larger datasets. Hybrid setups mix both, which is usually where things get interesting.

Overview of Different Types of Credit Scores

Credit scores are numerical representations that condense your credit history and financial behavior into a three-digit number. In practice, different lenders care about different versions of that number. One bank may lean hard on FICO. Another may prefer a custom score tied to its own portfolio.

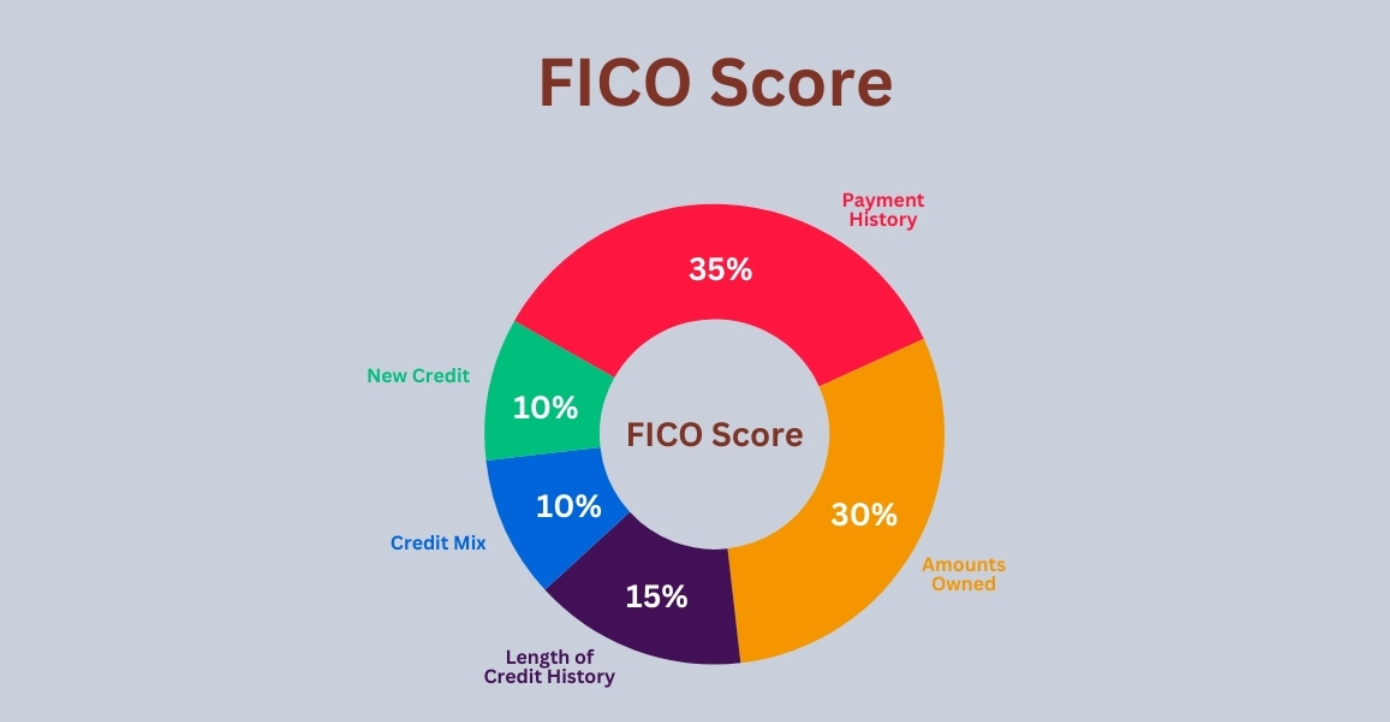

- FICO Score:

Developed by the Fair Isaac Corporation, FICO scores are still the standard a lot of lenders compare against. They range from 300 to 850, and higher usually means lower perceived risk. Mortgage teams, card issuers, and auto lenders use them constantly.

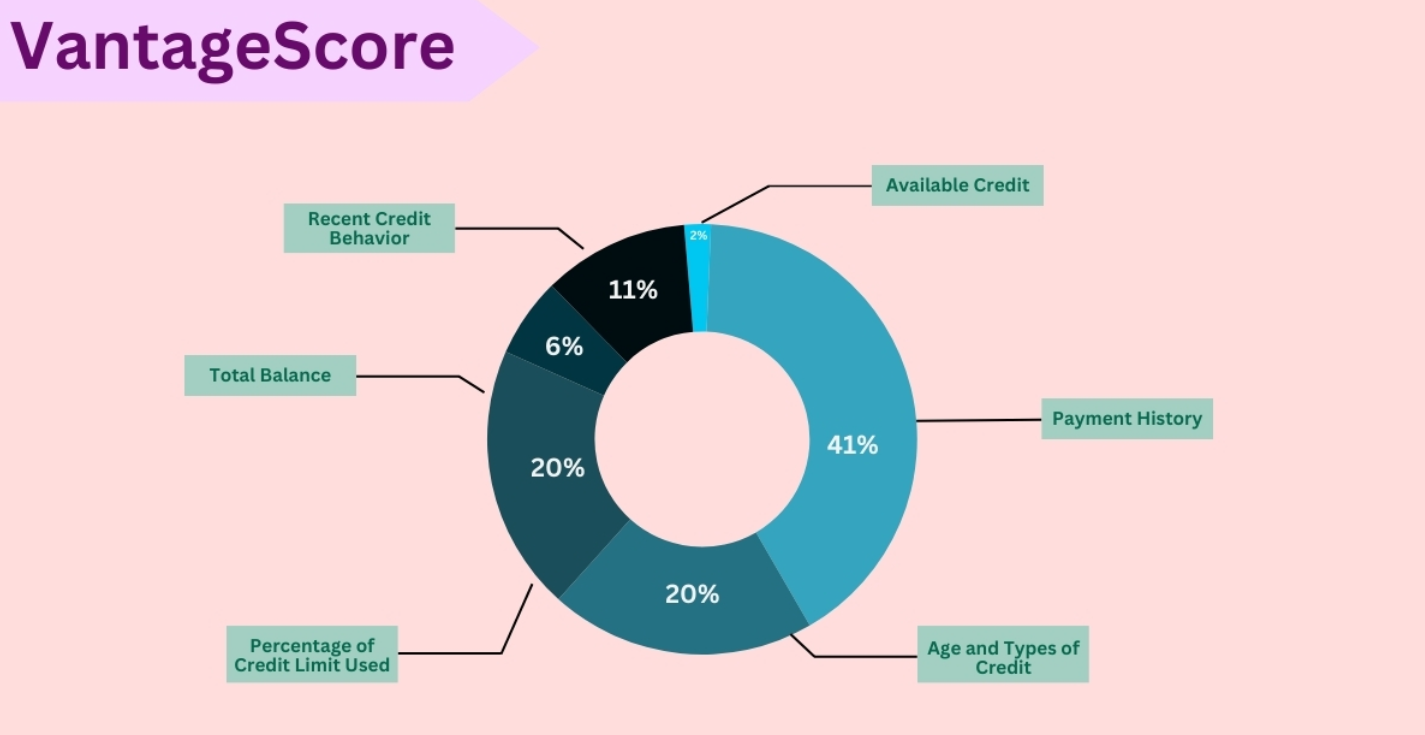

- VantageScore:

VantageScore was introduced by the three major credit bureaus: Experian, Equifax, and TransUnion. It also runs from 300 to 850. A lot of lenders use it when they want a slightly different view of the same borrower.

- Industry-Specific Scores:

Some sectors use their own variants. Auto lending is a common example, since repayment behavior there does not always line up neatly with a mortgage-style score.

- Customized Scores:

Some lenders build proprietary scoring models around the signals that matter most to them. This is common in portfolio lending and fintech underwriting, where off-the-shelf scores do not always fit the risk appetite.

Knowing which score is being used matters. A borrower can look strong in one system and average in another. That mismatch is normal.

Types of Credit Scoring Models

Credit scoring models have moved well beyond the old bureau-only setup. Some are built for consistency. Others are built for prediction. A few try to do both, which is where the trade-offs start showing up.

Traditional Credit Scoring Models

Traditional models use standard credit bureau data and fixed scoring rules to estimate risk. FICO is the obvious example. Payment history, credit utilization, length of credit history, credit mix, and recent credit activity. Mortgages, credit cards, personal loans, and most legacy lending workflows.

Behavioral Scoring Models

Behavioral models look at how a borrower acts over time, not just their static credit profile. They are often updated with fresh account activity. Transaction patterns, repayment behavior, account activity, delinquency trends, and spending shifts. Existing customer monitoring, portfolio management, limit increases, and early warning systems.

Application Scoring Models

Application scoring models are built to evaluate a borrower at the point of application. They focus on whether the loan should be approved right now. Application details, credit bureau data, income, employment, and other submitted financial information. Instant loan approvals, credit card applications, BNPL checks, and digital onboarding.

Machine Learning-Based Models

These models use machine learning to find patterns in large datasets that rule-based systems can miss. They are usually stronger on prediction, not always on explainability.Bureau data, behavioral signals, alternative data, and large historical lending datasets. Fintech underwriting, fraud-linked risk checks, thin-file borrowers, and high-volume lending decisions.

Hybrid Scoring Models

Hybrid models combine rule-based scoring with machine learning or alternative data. They are often used when teams want better prediction without losing control.

Traditional credit data, behavioral inputs, alternative data, and model outputs from ML systems. Risk-sensitive lending, layered decisioning, and workflows where compliance still matters.

This is where a rules engine helps. It gives lenders a way to keep the model adjustable without turning every change into a full engineering task.

Implementing Credit Scoring with Nected

Implementing credit scoring with Nected means you can mix different scoring approaches without rebuilding the whole decision flow every time. It fits well when a team wants rules, flexibility, and fewer hard-coded decisions.

Watch a detailed and dedicated credit scoring implementation on Nected.

Adaptability Across Models

Nected works across traditional, machine learning-based, and alternative scoring setups. Users can configure rules for different lending policies without rewriting the whole stack. That matters when risk teams keep changing the thresholds, which they usually do.

Seamless Integration with Connectors

Nected also connects with tools like Redshift, so machine learning outputs and stored data can feed the scoring logic. That makes it easier to combine historical patterns with live decisioning instead of treating them like two separate systems.

Efficiency in Implementation

The interface is built so teams can define rules, set parameters, and adjust scoring criteria without heavy coding. That saves time when credit policies change or new borrower segments need different treatment.

In other words, Nected gives you room to work with both legacy scoring and newer decisioning setups. It is not magic. It just removes a lot of friction.

Elevate your credit scoring game today. Signup Now!

What Challenges in Credit Scoring Models Nected Solves

Credit scoring runs into the same problems over and over: messy data, new data sources, and models that become stale too quickly. Traditional systems can miss useful signals. Machine learning systems can be harder to explain. This is where things usually break.

Nected's Solutions

Nected tackles those gaps with a more controlled scoring setup. The point is not just to score faster. It is to keep the logic understandable while still handling more data.

- Data Accuracy Assurance:

Validation checks help keep bad inputs from slipping through. That matters more than it sounds, because a scoring model is only as good as the data feeding it.

- Handling Alternative Data Sources:

Nected can work with non-traditional inputs like rental history or utility payments. That gives lenders a broader view of borrowers who do not have deep bureau files.

- Interpretability in Machine Learning Models:

Machine learning can improve prediction, but it often leaves teams guessing about why a decision was made. Nected keeps the scoring logic easier to inspect, which helps when compliance or internal review gets involved.

- Adaptability to Evolving Requirements:

Credit policies do not stay still for long. Nected makes it easier to update rules as underwriting standards, risk appetite, or regulations shift.

So it is not just a credit scoring platform. It is also a way to keep the process from turning into a maintenance headache.

Conclusion

Different credit scoring models solve different problems. Traditional models are stable. Behavioral models watch what borrowers do next. Machine learning models push harder on prediction. Hybrid setups try to balance control and accuracy. The right choice depends on the lending use case, not just the model name.

Nected fits into that picture by making scoring logic easier to manage without losing flexibility. For teams dealing with changing credit rules, that is often the part that matters most.

FAQs

What is a credit scoring model?

A credit scoring model is a system that estimates how risky a borrower is based on financial data, credit history, and related signals.

What are the types of credit scoring models?

The main types are traditional credit scoring models, behavioral scoring models, application scoring models, machine learning-based models, and hybrid scoring models.

Which credit scoring model is best?

There is no single best model. Traditional models work well for standard lending, while machine learning and hybrid models are better when you need more predictive power or broader data coverage.

How do credit scoring models work?

They collect borrower data, apply scoring rules or statistical models, and turn that into a score or risk decision lenders can use.

.svg.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)