.png)

.webp)

In today's world, getting loans or credit cards matters a lot when you're buying a house or starting a business. The problem is that traditional scoring systems still miss a lot of people. If someone has thin credit history, irregular income, or just doesn't fit the usual pattern, they can get filtered out fast. That's where open source credit scoring software starts to make sense.

It gives teams a way to build and adjust their own credit scoring engine instead of being boxed into a fixed vendor model. The code is open, the logic is easier to inspect, and the whole setup is usually less rigid. That part often gets ignored.

If you're trying to understand how open source credit scoring software fits into lending and risk decisions, the sections below cover the basics without dragging it out.

What Is a Credit Scoring Engine?

A credit scoring engine is the part of a lending system that takes borrower data and turns it into a risk score. Lenders use that score to decide whether someone looks safe enough to approve, how much credit to offer, and sometimes what terms to attach.

It sits between the raw data and the final decision. The scoring model does the math. The engine runs that model, applies rules, and pushes the result into the decisioning flow. In practice, lenders look at payment history, debt load, income signals, and a few other things that matter to their portfolio.

That is why the relationship between the scoring model and the engine matters. The model is the logic. The engine is the system that makes it usable in production.

What is open source credit scoring software?

Open source credit scoring software is a freely available tool that lenders and fintech teams can use, modify, and distribute. Unlike proprietary credit scoring software, which stays locked behind a vendor, open source code gives teams more control over how scoring works.

These tools assess creditworthiness using financial factors like payment history, debt levels, and income. Many of them rely on an open source credit scoring engine to run rules, models, and score calculations without forcing everything into a black box.

That makes the credit assessment process easier to adapt. A bank, a BNPL provider, and a microfinance platform will not evaluate risk the same way, and they usually should not. Open source software gives them room to tune the logic instead of starting from scratch.

What is the Importance of Open Source Credit Scoring Softwares?

The value of open source credit scoring software comes from what it fixes. Traditional systems can be expensive, opaque, and hard to adapt. Open tools solve some of that, though not magically.

- Financial Inclusion: They help lenders assess people who don't fit standard bureau-driven models. That includes borrowers with little or no credit history.

- Democratization of Credit Scoring: Smaller institutions can access credit scoring software without paying for heavy enterprise licensing.

- Innovation and Collaboration: Teams can test new data sources and rules faster. This is where things usually break in closed systems.

- Increased Transparency and Trust: Open logic is easier to inspect, which helps when regulators or internal risk teams want answers.

- Expansion of Financial Inclusion: Alternative data and custom scoring approaches can widen credit access for underserved groups.

- Challenges to Traditional Models: Open source tools push vendors to compete on usability and model quality instead of just branding.

Credit Assessment Software Explained

Credit assessment software is what lenders use to evaluate financial risk before approving credit. It looks at borrower signals, applies scoring models, and helps sort applicants into different risk bands. The output is rarely just a single number. It usually feeds a broader decision process.

This kind of software shows up in lending platforms, BNPL systems, and risk management systems. In each case, the goal is the same: figure out whether the borrower can handle the obligation and whether the exposure makes sense for the business.

It overlaps with credit scoring software, but the scope is often wider. Some systems only score. Others combine rules, policy checks, and model outputs in one place.

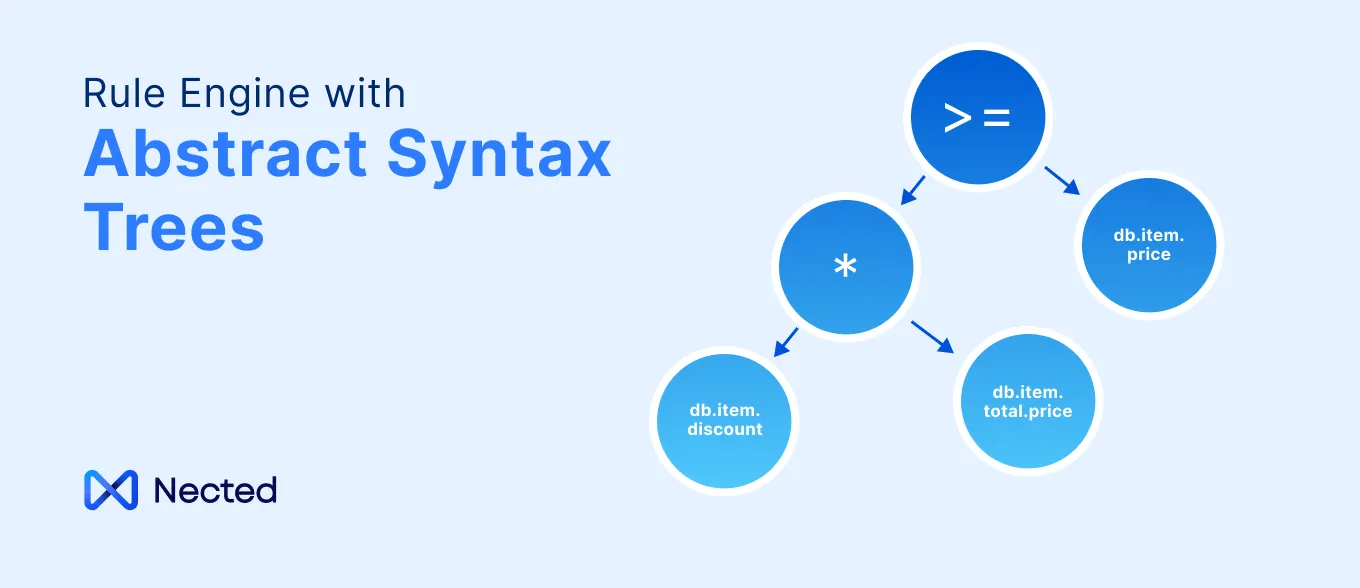

Credit Scoring Engine Architecture

A credit scoring engine usually has a few moving parts. There is a data intake layer, a rules layer, a scoring model layer, and a decision output layer. Some setups also include audit logs and monitoring because lenders need to track why a decision happened.

Data comes in from applications, bureau pulls, bank statements, or alternative sources. The engine then cleans that data, applies rules, runs the score, and sends the result to underwriting or approval workflows. If the architecture is messy, the whole thing becomes hard to trust. This part often gets ignored until production starts failing.

In better setups, the engine is modular. That makes it easier to swap models, adjust thresholds, and keep compliance teams happy without rebuilding everything.

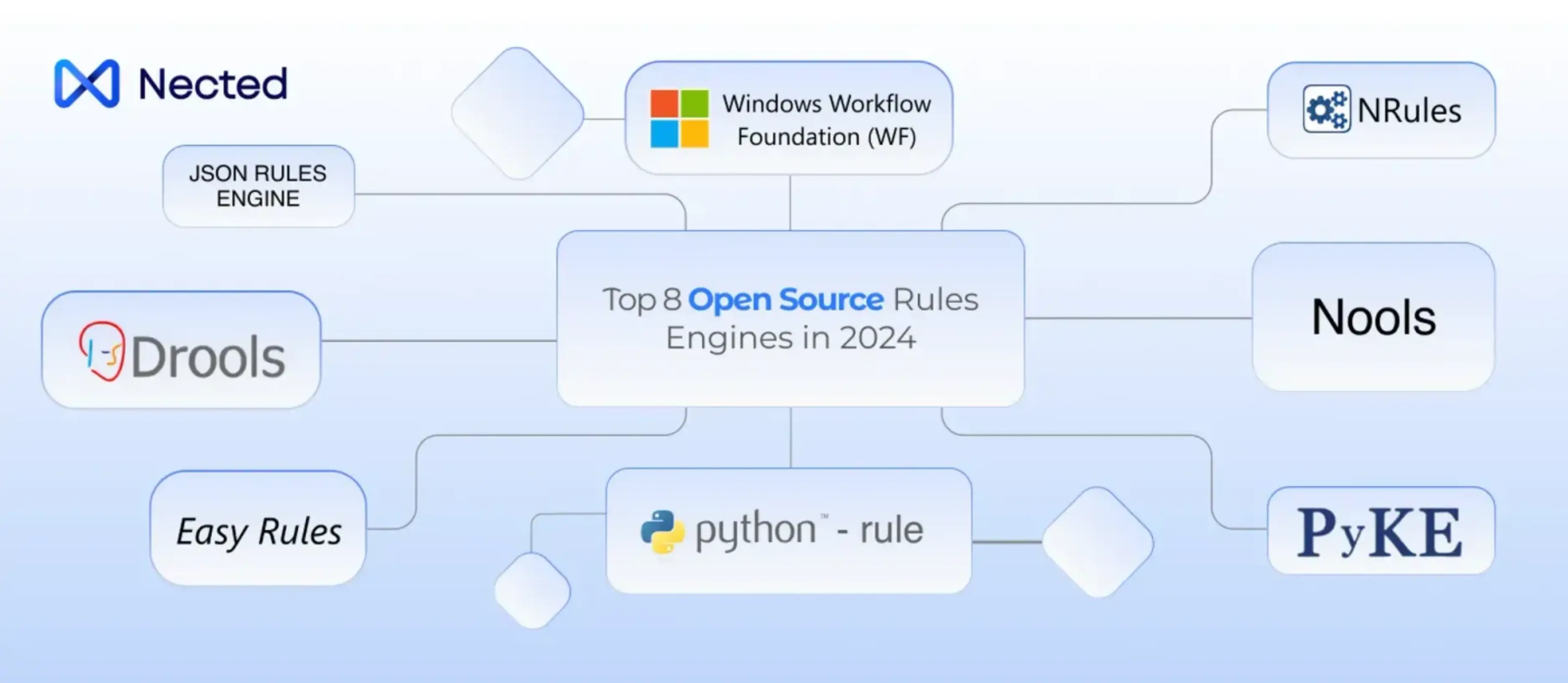

Top Open Source Credit Scoring Engines

There's no single "right" tool here — it depends on your team's technical depth, how often rules change, and whether you need something production-ready out of the box or are fine building around a core library. Here are five tools teams commonly look at when building lending workflows.

1. FICO Open Source Scorecard

If your team is coming from a traditional credit background, scorecard-style tools feel familiar. The logic is straightforward — weight variables, sum scores, apply cutoffs. Easy to explain to stakeholders, easy to audit.

Key Features:

- Traditional scorecard model support

- Variable weighting and binning

- Output is interpretable score ranges

- Works well in analytical and batch environments

Use Cases:

- Consumer lending

- Credit risk tiering

- Portfolio-level risk assessment

Pros:

- Interpretable by default — regulators and risk teams understand scorecards

- Low barrier to entry for teams with existing scoring expertise

- Good for batch processing workflows

Cons:

- Not designed for real-time decisioning at scale

- No native workflow or automation layer — you're building that separately

- Updating models means redeployment, which slows iteration

2. Nected

Nected is a low-code/no-code decision management platform built for rule execution, workflow automation, and experimentation. It's the strongest pick here if you want something that works for both technical and non-technical teams — without turning every rule change into a dev task.

What sets it apart from the others on this list is that it's not just a scoring library. It's a full decisioning environment. You can define credit rules, chain them together, connect to external data sources, and run experiments — all without touching application code for most changes. That matters a lot when your underwriting logic is evolving frequently.

Key Features:

- Rule-based and decision-driven scoring model support

- Visual rule editor — no SQL or code required for routine changes

- Rule chaining for multi-step underwriting logic

- Real-time rule execution with minimal latency

- API and database integrations out of the box

- Built-in version control and audit trails

- Cloud and self-hosted deployment options

- Workflow automation that goes beyond just rule evaluation

Use Cases:

- Loan approval workflows

- Fintech lending decisioning

- Credit risk assessment and tiering

- Behavioral scoring

- Underwriting logic management

Pros:

- Business teams can manage and update rules without engineering involvement

- Speeds up iteration on scoring logic significantly

- Handles both rules and workflow in one platform — fewer tools to manage

- Scales without the architecture getting heavy

- Audit trails make compliance easier

- Supports experimentation — you can test rule changes before rolling them out

Cons:

- Advanced features take some time to get comfortable with

- Teams coming from very old or fragmented legacy systems may need extra integration work upfront

Nected is the practical choice when you want decisioning control without the overhead of building everything yourself. It sits between a raw ML library and a full enterprise decisioning suite — useful without being overbuilt.

3. scikit-learn Based Scoring Stack

Scikit-learn isn't a credit scoring engine. It's a machine learning library that teams use to build one. That distinction matters. If you go this route, you're assembling the scoring pipeline yourself — model training, serving, rule integration, monitoring. The library handles the ML part. Everything else is on you.

That said, it's one of the most widely used tools in data science for a reason. The documentation is excellent, the community is large, and it plays well with the rest of the Python ecosystem.

Key Features:

- Support for logistic regression, decision trees, gradient boosting, and other common credit models

- Easy integration with custom rule layers

- Works with pandas, NumPy, and standard Python data tooling

- Flexible deployment — can be wrapped in an API or integrated into pipelines

Use Cases:

- Custom credit scoring model development

- Fintech lending experimentation

- Risk model prototyping

Pros:

- Widely understood — most data science teams know it already

- Extremely flexible for model experimentation

- Easy to iterate on model development

Cons:

- Not a complete solution — you're building the surrounding workflow yourself

- No native decision management layer

- Deployment and serving need to be handled separately

- Not accessible to non-technical teams at all

4. R / Scorecard Package

The scorecard package in R is built specifically for traditional credit scorecard development — Weight of Evidence (WoE) binning, Information Value (IV) calculations, logistic regression scoring. If your team lives in R and does a lot of statistical analysis alongside model development, this fits naturally.

Key Features:

- Scorecard model development with WoE and IV support

- Binning and variable selection tooling

- Can integrate with internal analytics stacks

- Good for batch scoring and portfolio analysis

Use Cases:

- Traditional scorecard development

- Portfolio risk reporting

- Regulatory model documentation

Pros:

- Purpose-built for scorecard methodology

- Outputs are interpretable and documentable

- Good fit for teams with a strong statistical background

Cons:

- R-specific — limits who on your team can work with it

- Not suited for real-time decisioning

- No automation or workflow capabilities

- Updating and redeploying models requires technical involvement every time

5. H2O.ai (Open Source)

H2O's open source platform handles automated machine learning, which makes it interesting for teams that want to build more sophisticated credit models without writing everything from scratch. AutoML can run through multiple model types and surface the best performers — useful during model selection.

Key Features:

- AutoML for automated model comparison and selection

- Support for gradient boosting, random forests, neural networks

- Model interpretability tools (SHAP values, variable importance)

- REST API for model serving

- Can be run locally or on a cluster

Use Cases:

- Advanced credit risk modeling

- Default probability prediction

- Alternative data scoring

Pros:

- AutoML reduces time spent on model selection

- Handles larger datasets reasonably well

- Interpretability features help with model explainability

- Open source core is genuinely capable

Cons:

- Steeper learning curve than scikit-learn for teams less familiar with it

- Still needs a separate decisioning and workflow layer in production

- Enterprise features require a paid license

- Not accessible to non-technical stakeholders

A detailed comparison between Nected and other credit scoring tools

The tools that are purely ML libraries — scikit-learn, H2O, the R scorecard package — are capable for model development, but they don't solve the decisioning problem on their own. You still need something to manage rules, handle workflow, run experiments, and give non-technical teams visibility into what's happening.

That's the gap Nected fills. It's not trying to replace your data science stack. It's the layer that sits on top and makes the decisions actually operational — without requiring a developer for every update.

Benefits of Using Credit Scoring Engines

A good credit scoring engine does more than spit out a number. It shortens approval time, reduces manual review, and gives lending teams a cleaner way to control risk. That matters when volume starts climbing.

- Faster lending decisions: Applications can move through the flow without waiting on manual checks.

- Reduced risk: Better scoring means fewer bad approvals.

- Automated underwriting: Rules and scores can work together instead of living in separate systems.

- Improved compliance: Decision trails are easier to audit when the engine is built properly.

Key features and functionalities of Nected

- Accessibility and Ease of Use: Nected is built with a simple interface, so teams don't need to wire everything by hand just to get a score flow running.

- Flexibility and Customization: You can tune rules, logic, and data inputs to match your lending policy instead of forcing the policy to fit the tool.

- Transparency and Openness: The decision path is easier to inspect, which helps when internal teams want to understand why a score moved a certain way.

- Cost-Effectiveness: It avoids the kind of licensing cost that makes smaller lenders hesitate.

- Innovation and Collaboration: Different teams can work on models, rules, and monitoring without stepping on each other.

Use Cases of Credit Scoring Software

Open source credit scoring software shows up in a lot of places once teams move beyond plain vanilla lending.

- Personal loan approval: Useful when lenders need to approve applications quickly and keep risk under control.

- SME lending: Helpful for small business lending, where bureau data alone usually doesn't tell the full story.

- BNPL platforms: Short-term lending needs quick decisions, and the scoring engine has to be fast.

- Credit card approvals: Card issuers use scoring to sort applicants and set limits.

- Risk monitoring: Some teams use the same software after approval to watch for changes in borrower behavior.

Real-Life Credit Scoring Implementation with Nected

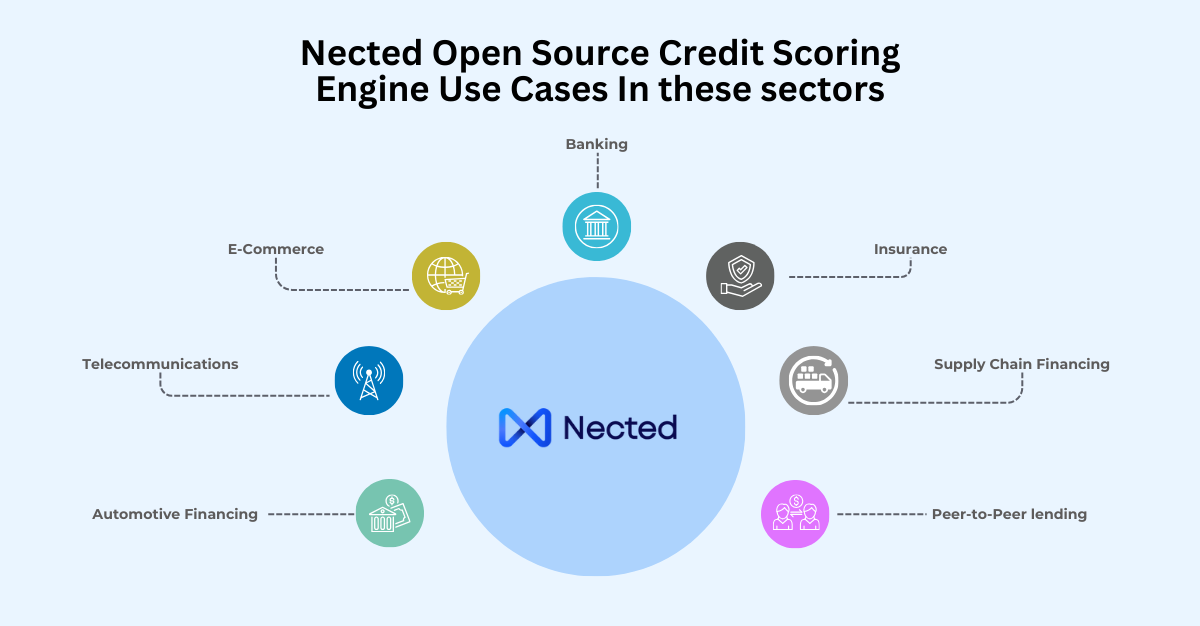

Nected can assist you in building credit scoring systems tailored to different industries and purposes:

- Automotive Financing: It can be used to build credit scoring models for auto loan eligibility. Better scores often mean better loan terms, and that part is pretty standard.

- Telecommunications: Mobile service providers use scoring to decide whether a customer should get a postpaid plan or stay on prepaid.

- Online Retailers: eCommerce platforms use behavioral credit scoring for financing options and buy-now-pay-later programs.

Apart from the sectors mentioned above, the tool can also be used in banking, insurance, fintech, p2p lending, microfinance, and supply chain financing, where credit assessment is part of the workflow.

For a step-by-step guide on using Nected for behavioral credit scoring, see this article: Mastering Credit Scoring with Nected.

Conclusion

Open source credit scoring software gives lenders more control over how they assess risk. It makes credit decisions easier to inspect, easier to customize, and, in a lot of cases, easier to scale without vendor lock-in.

That is especially useful when you need a credit scoring engine that can adapt to different borrower types or lending products. The same logic also applies to credit assessment software, where the real value is in matching decisioning to the business instead of forcing the business to match the tool.

If you're planning to build or adjust a behavioral credit scoring system, Nected is worth a look. It lets you build tailored models using the data points that actually matter for your workflow.

Start with Nected if you need a credit scoring tool that gives you more control without making the whole process messy.

FAQs

What is a credit scoring engine?

A credit scoring engine is the system that takes borrower data, applies scoring logic, and returns a credit risk result lenders can use in approval or underwriting.

What is open source credit scoring software?

It is credit scoring software whose source code is available to view, modify, and distribute. Teams use it when they want more control over scoring logic and deployment.

How does credit assessment software work?

It evaluates borrower data, runs scoring models, and helps lenders estimate financial risk before making a decision.

What are the best credit scoring tools for fintech companies?

The best credit scoring tools depend on the use case. Fintech teams usually look for a mix of scoring model support, rule engine integration, deployment flexibility, and auditability.

.svg.webp)

.webp)

_result.webp)

.webp)

%20(1).webp)